Construction equipment financing in Cambridge explained: lease structures, approvals, HST, used equipment, underwriting, and contractor cash-flow tips.

Construction equipment financing in Cambridge helps contractors acquire excavators, skid steers, loaders, compactors, telehandlers, trailers, lifts, pavers, trenchers, and other heavy equipment without draining working capital. The best structure is usually leasing-first: match the payment to the equipment’s useful life, contract revenue, seasonality, down payment, residual value, and resale strength.

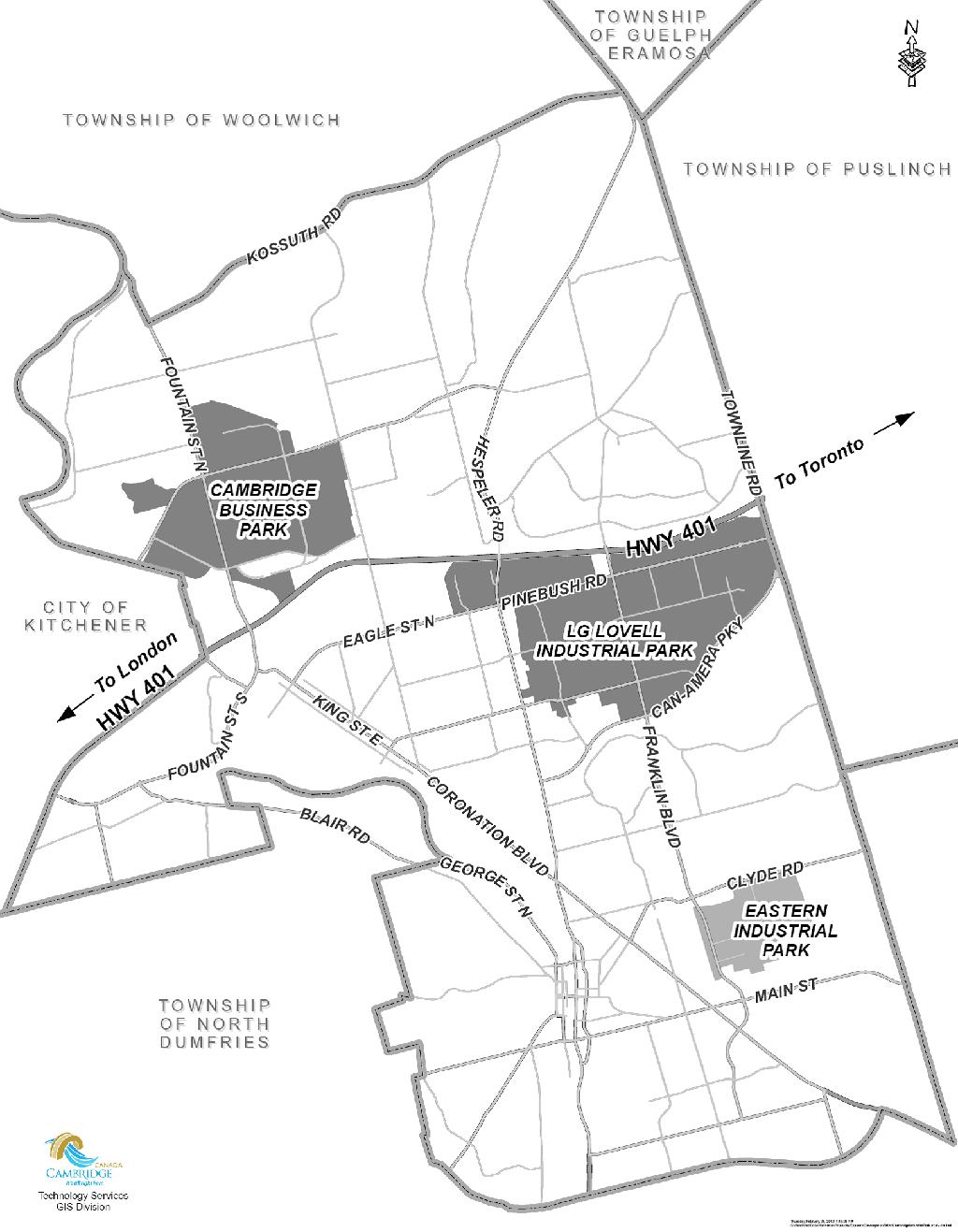

Cambridge is a practical equipment market because local contractors work around industrial parks, logistics corridors, infrastructure upgrades, residential development, commercial builds, and manufacturing facilities. Highways 401, 8, and 24 run through the city, and Cambridge has five interchanges to Highway 401, giving contractors and haulers access to major routes from local industrial areas. (Invest Cambridge)

Construction equipment financing matters because contractors often need the machine before the contract cash arrives. A lease or structured equipment facility can protect cash for payroll, fuel, insurance, repairs, deposits, permits, and supplier terms.

Cambridge contractors serve more than one type of demand. Local work can include site servicing, road work, grading, residential subdivisions, commercial renovations, manufacturing plant upgrades, warehousing projects, utility work, landscaping, concrete, paving, and snow operations. The city is also an advanced manufacturing hub, with advanced manufacturing accounting for nearly 20% of Cambridge’s workforce, which creates demand for contractors supporting industrial facilities, maintenance, expansions, and site improvements. (City of Cambridge)

A contractor buying a $125,000 skid steer, $240,000 excavator, or $450,000 loader should not treat the purchase like a one-time bill. The real question is whether the machine can earn enough, often enough, to support the payment through slow months and weather delays.

Start with Mehmi’s page on construction equipment financing, then compare it against broader equipment leasing structures when the asset and job pipeline are clear.

Construction equipment financing usually means a lender funds the asset and your business repays over a set term. In practice, most contractor deals are structured like leases because the equipment itself is the main collateral.

The funder looks at the machine, the borrower, the vendor, the down payment, the term, and the repayment source. If approved, the lender pays the vendor or seller, and the contractor makes scheduled payments. At the end, the business may own the asset, buy it out, renew, trade up, or return it depending on the structure.

Common structures include finance leases, conditional sale-style structures, operating or residual leases, seasonal payment plans, used-equipment leases, private-sale financing, and refinancing or sale-leaseback. The right one depends on cash flow and asset life.

A leasing-first approach does not mean the cheapest payment at all costs. It means the structure should fit how the machine earns revenue.

Local context matters because lenders want to understand where the equipment will work, how it will be used, and whether demand is realistic. In Cambridge, transportation access, construction disruption, industrial activity, and municipal approvals can all affect timing.

First, Cambridge’s road network matters. Highway 401 access supports contractors who move machines between Cambridge, Kitchener, Waterloo, Guelph, Brantford, Milton, and the GTA. It also makes float trailers, service trucks, compact equipment, and multi-site scheduling more important than in a purely local market. Cambridge’s transportation profile specifically highlights Highways 401, 8, and 24 and access from industrial areas. (Invest Cambridge)

Second, local road and infrastructure projects can create both opportunity and operational friction. The City of Cambridge maintains a road construction project page for current projects, and contractors should track active work and detours when planning equipment utilization. (City of Cambridge) The Region of Waterloo’s Can-Amera Parkway project, updated in February 2026, includes asphalt replacement, multi-use paths, bus stop improvements, lighting, and guiderail replacement between Conestoga Boulevard and Franklin Boulevard. (Region of Waterloo)

Third, municipal permits can affect when a project starts. Cambridge’s building permit portal allows users to submit and track permit applications, make payments, and request permit information. (City of Cambridge) If equipment is being purchased for a specific project, lenders like to know whether the job is awarded, permitted, staged, and funded.

Fourth, Cambridge licensing can matter for some operators. The City says most businesses in Cambridge must be licensed to operate legally. (City of Cambridge) Contractors with regulated activities, commercial yards, mobile operations, or related business categories should make sure licensing is current before applying.

Most revenue-producing construction equipment can be financed if it has a clear use, identifiable value, and enough useful life. Lenders prefer hard assets that can be inspected, insured, registered where applicable, and resold.

Common equipment includes excavators, mini excavators, skid steers, compact track loaders, wheel loaders, backhoes, bulldozers, motor graders, rollers, compactors, pavers, trenchers, telehandlers, scissor lifts, boom lifts, compressors, generators, light towers, concrete equipment, dump trailers, equipment trailers, water trucks, service bodies, and vocational units.

Are you looking for a truck? Look at our used inventory (https://www.mehmigroup.com/inventory).

Brand, hours, maintenance, application, and attachments matter. A mainstream excavator from a major manufacturer with clean service history is easier to underwrite than a highly modified unit with unclear hours, missing serial numbers, or poor resale support.

For related asset categories, contractors can also compare heavy equipment financing, trailer financing, and commercial truck financing.

Used equipment can be smart when the machine has enough remaining life and the payment is low enough to protect cash flow. New equipment can be better when warranty, uptime, technology, and resale value are critical.

A practical example: a Cambridge excavation contractor may lease a new compact track loader for daily work but buy or finance a used roller that is used less frequently. That can be smarter than putting every asset on the newest, most expensive structure.

Mehmi’s guide to new vs used equipment financing in Canada is a useful supporting read before comparing quotes.

The lease-vs-buy decision should start with working capital, not pride of ownership. Paying cash for equipment can look responsible but weaken the business if it leaves the contractor short for labour, fuel, repairs, insurance, or job deposits.

Leasing can be better when the equipment will generate revenue over several years, cash must be preserved, the contractor wants predictable payments, or the asset may be upgraded. Buying can be better when the equipment is inexpensive, cash reserves remain strong after purchase, and the contractor plans to use the machine for a long time.

My direct opinion: contractors often overestimate ownership value and underestimate cash-flow risk. Owning a paid-off excavator is great. Owning it while missing payroll or delaying supplier payments is not. The healthiest contractors usually finance the asset over the period it earns money and keep cash available for job execution.

For a deeper comparison, use Mehmi’s guide to equipment leasing vs buying in Canada.

Lenders underwrite two things: the contractor and the machine. A strong asset helps, but cash flow still needs to support repayment.

The common credit framework is the 5Cs: character, capacity, capital, collateral, and conditions. Character is repayment history and owner conduct. Capacity is whether the business can afford the payments. Capital is the owner’s investment and equity in the business. Collateral is the equipment and supporting security. Conditions include the construction market, job pipeline, seasonality, rate environment, and the purpose of the equipment. The uploaded credit-risk reference describes 5C analysis as character, capacity, capital, collateral, and conditions.

Behind the scenes, lenders also think about probability of default, exposure at default, and loss given default. In plain English: how likely is the contractor to miss payments, how much will still be owing, and how much can be recovered from the machine, guarantees, insurance, or other collateral.

That is why a $300,000 excavator request may get different answers from two similar-looking contractors. One has signed work, clean bank statements, documented experience, and a mainstream asset. The other has thin deposits, no job details, an older machine, and unclear repayment. Same equipment type, different risk profile.

A strong construction equipment financing application explains how the machine will pay for itself. Lenders are more comfortable when the equipment is tied to contracts, capacity, replacement savings, or measurable revenue.

Include the equipment quote, business history, owner experience, job pipeline, top customers, current fleet, existing debt, bank statements, and expected monthly utilization. For replacement equipment, explain what is being replaced and why. For additional equipment, explain the added revenue or cost savings.

The uploaded credit guideline reference says applications should include equipment details such as make, model, year, hours or kilometres, whether it is new or used, a brief summary of activity sector, years in business, reason for financing, and desired structure such as term, down payment, and residual.

For construction files, the lender wants to know:

Who are the main customers?

Is the work residential, commercial, municipal, industrial, or civil?

Is the equipment additional or replacement?

What contracts or jobs support the need?

How many machines are already in the fleet?

Who services the equipment?

What is the seasonal plan?

How will downtime be handled?

If the contractor is new, the owner’s prior sector experience becomes more important. If the equipment is old, hours, service records, and repair invoices matter more.

Down payment and term should reflect risk, equipment age, and cash flow. A low down payment is helpful only if the resulting payment still fits the business.

Newer mainstream construction equipment may qualify for longer terms, while older assets may have shorter terms because lenders do not want the financing to outlast the equipment’s useful life. Higher hours, specialized attachments, weak credit, limited time in business, or private sales can all increase down payment expectations.

Residuals can reduce the payment, but they must be realistic. Residual risk is about what the equipment will be worth at the end of the lease. A strong residual can make sense for high-demand assets, but it is dangerous if the projected value is too optimistic.

The uploaded lender reference for construction equipment notes that construction equipment residual programs may apply to specific equipment types and that residuals can depend on asset type, manufacturer tier, and whether the equipment is new or low-use demo equipment.

For contractors acquiring several assets at once, read Mehmi’s guide to financing multiple pieces of equipment at once in Canada.

A complete package prevents delays. Many construction equipment deals slow down because the quote is incomplete, the seller is unverified, the serial number is missing, or the insurance certificate is not ready.

Prepare:

Business registration or articles of incorporation.

Recent business bank statements, usually three to six months.

Government ID for signing owners or guarantors.

Equipment quote or invoice with year, make, model, serial number, hours, and attachments.

Photos for used equipment, especially all sides and hour meter.

Proof of ownership and lien search for private sales.

Repair history or inspection for older machines.

Current financial statements for larger requests.

Job letters, contracts, purchase orders, or revenue support where available.

Insurance certificate showing lender requirements.

Void cheque or PAD form.

Proof of down payment, if required.

A short write-up explaining why the equipment is needed.

For private-sale equipment, expect more scrutiny. The lender needs to confirm the seller owns the asset, the asset is free of liens or can be paid out, and the equipment exists in the represented condition.

Ontario contractors need to plan for HST timing. Even when GST/HST input tax credits are available, the timing can affect cash flow.

As of May 2026, CRA guidance says registrants can generally claim input tax credits only for the part of GST/HST paid or payable that relates to consumption or use in commercial activities. (Canada) For equipment financing, that means documentation, business use, invoice accuracy, and filing timing matter.

The Canada-specific gotcha is that a great approval can still create cash stress if HST is not planned. A contractor leasing equipment may pay HST on payments. A contractor buying through a different structure may have a larger upfront tax timing issue. The right structure should consider both payment and tax cash flow.

Before signing, compare Mehmi’s guide to GST/HST input tax credits on financed equipment in Canada and confirm treatment with your accountant.

Interest rates affect equipment payments, but they are only one part of pricing. Credit strength, asset type, term, down payment, age, hours, vendor, and lender appetite also matter.

As of April 29, 2026, the Bank of Canada held the target overnight rate at 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%. (Bank of Canada) That does not tell you your exact lease rate, but it helps explain the broader cost-of-capital environment.

Contractors should stress-test payment in real terms. Ask whether the payment works if a project is delayed, receivables pay 30 days late, fuel rises, repairs hit, or winter revenue slows. If the equipment only works financially in a perfect month, the structure is too tight.

The Canada Small Business Financing Program can sometimes support equipment purchases, but it is not always the fastest or most flexible route for contractors.

As of May 2026, ISED says the Canada Small Business Financing Program makes it easier for small businesses to get loans from financial institutions by sharing risk with lenders. (ISED Canada) ISED’s CSBFP guidelines state that within the program maximums, up to $500,000 can be used for purposes other than real property, including equipment and leasehold improvements, with up to $150,000 inside that limit for intangible assets and working capital costs. (ISED Canada)

For Cambridge contractors, CSBFP may be worth comparing if the project involves equipment, leasehold improvements, or broader business expansion. But if the goal is fast heavy equipment funding, used equipment, private sale, seasonal payments, or refinancing, a conventional equipment lease may fit better.

Mehmi’s Canada Small Business Financing Program guide explains where it fits.

Approval does not always mean same-day funding. Lenders may still need documents, proof, insurance, and security before money is advanced.

Conditions precedent are requirements that must be satisfied before funding. In a construction equipment deal, examples include signed lease documents, verified invoice, insurance certificate, lien search, registration, down payment proof, inspection, or delivery and acceptance.

Covenants are rules monitored after funding. Smaller leases may have light covenants. Larger or higher-risk files may require financial statements, proof of insurance renewal, tax compliance, reporting on major contracts, or limits on selling or moving the equipment without consent.

The uploaded commercial lending reference explains that conditions precedent are items a borrower must comply with before funds are lent, while covenants help a lender monitor performance after lending; it also notes that prudent lenders prefer to spot warning signs before missed payments occur.

Monitoring is practical. Lenders watch for missed payments, NSF items, cancelled insurance, tax arrears, declining bank deposits, loss of major contracts, equipment misuse, unauthorized sale, or stacking high-cost debt.

A Cambridge site-preparation contractor had steady work with builders and small commercial clients. The owner wanted to add a used 20-ton excavator and a new compact track loader. The total equipment package was approximately $410,000.

The original request was for the lowest possible monthly payment with minimal money down. On review, the issue was not approval alone. The contractor had good revenue, but receivables often paid late, and winter months were slower. A low-down, long-term structure would have left very little room for fuel, payroll, repairs, and float costs.

The deal was restructured. The excavator received a term matched to its age and hours, with service records and an inspection included. The compact track loader was financed separately with a stronger residual profile. The owner provided bank statements, job pipeline details, current fleet list, proof of insurance, and a short explanation showing how the added equipment reduced subcontractor costs and allowed the company to run two crews.

From the lender’s view, the 5Cs were clear. Character was supported by clean repayment history. Capacity was supported by deposits and job pipeline. Capital was supported by a reasonable down payment. Collateral was strong because both machines had resale value. Conditions made sense because Cambridge and the surrounding Waterloo Region market had ongoing infrastructure, industrial, and site-work demand.

The contractor did not just get equipment. They got a payment structure that protected working capital.

Sometimes the contractor does not need new equipment. They need liquidity from equipment they already own.

A sale-leaseback can unlock cash from paid-off machines while the contractor continues using them. This may help fund deposits, payroll, tax cleanup, debt consolidation, or mobilization for a larger contract. It works best when the equipment has clear ownership, strong value, serial numbers, photos, insurance, and enough remaining useful life.

For example, a Cambridge contractor with paid-off skid steers and trailers may refinance part of that equity to support a large municipal or industrial job. That can be cleaner than stacking unsecured short-term debt.

Review Mehmi’s equipment refinancing and sale-leaseback options if owned equipment could support the next stage of growth.

Most equipment financing mistakes are structure mistakes, not equipment mistakes. Contractors often choose a machine they need but finance it in a way that stresses the business.

Avoid these common errors:

Financing an old machine over too long a term.

Ignoring inspection, maintenance, and repair reserves.

Assuming a signed quote equals approval.

Using working capital to buy equipment outright.

Taking the lowest payment without reading the end-of-term terms.

Buying equipment before confirming job timing.

Ignoring HST timing.

Adding equipment when labour capacity is the real constraint.

Using short-term cash advances for long-life assets.

For broader planning, Mehmi’s guide on how construction companies finance heavy equipment like excavators and loaders is a strong supporting resource.

The best next step is to package the equipment request like an underwriter would read it. Show the asset, the work, the cash flow, the repayment source, and the downside protection.

Create a one-page financing brief with the equipment description, vendor quote, total cost, down payment, desired term, equipment location, current fleet, job pipeline, top customers, revenue history, existing debt, and whether the asset is replacement or additional. Add local context where it helps: Highway 401 access, industrial customers, municipal or regional work, Cambridge job sites, or surrounding service area.

Mehmi can help compare construction equipment leasing, used-equipment financing, private-sale structures, refinancing, sale-leaseback, working capital, and asset-based lending. The goal is not just to secure the machine. The goal is to fund it in a way your contracting business can carry through busy months and slow ones.

Yes, but startups and newer contractors need stronger support. Lenders may ask for prior industry experience, bank statements, contracts or job letters, owner investment, personal credit, a clear equipment purpose, and a realistic cash-flow plan. New contractors should avoid overbuying before revenue is proven.

Yes. Used excavators, loaders, skid steers, trailers, lifts, and compactors can often be financed if the age, hours, condition, serial number, seller, and value make sense. Older equipment may require inspection, photos, service history, repair invoices, or a larger down payment.

It depends on credit, time in business, equipment age, asset type, seller, and term. Stronger files may qualify with lower down payments. Weaker credit, startups, private sales, older equipment, or specialized machines usually require more cash down.

Lease when preserving cash matters, the asset will earn over time, or you may upgrade later. Buy when the equipment is inexpensive, cash reserves remain strong, and the business can absorb repairs and slow months. For many contractors, leasing is safer because it protects working capital.

Yes, but lenders will look at total exposure, fleet size, utilization, revenue, and whether each asset has a clear purpose. A contractor financing an excavator, skid steer, trailer, and compactors should explain how each asset supports specific jobs or crew capacity.

Common delays include incomplete invoices, missing serial numbers, unclear ownership, unresolved liens, expired IDs, missing insurance, no proof of down payment, weak bank statements, private-sale documentation gaps, or an unclear reason for buying the equipment.

.avif)