Small business loans in Granby explained: working capital, lines of credit, factoring, leasing, CSBFP, tax timing, approvals, and lender requirements.

Small business loans in Granby can help local companies manage cash flow, buy equipment, renovate space, carry inventory, hire staff, launch a new location, or take on larger contracts. The right financing option depends on what the money is for, how fast revenue returns, and what a lender can verify.

Granby has a strong local business base, especially around manufacturing and industrial activity. Granby’s industrial development organization says the industrial park has more than 160 manufacturing companies, while the broader “Granby in Numbers” profile lists a population of 68,599 in Granby and 91,862 in Haute-Yamaska. (Granby Industriel)

Small business financing is not one product. It is a set of tools for different business problems.

A Granby manufacturer may need funds for raw materials before customer receivables are collected. A restaurant or retailer may need inventory, staffing, signage, or leasehold improvements before seasonal demand arrives. A contractor may need deposits, tools, vehicles, or payroll before progress payments come in. A distributor may need cash for supplier terms while serving customers across Montérégie, Estrie, Montréal, Sherbrooke, and the U.S. border corridor.

The strongest loan request starts with purpose. “We need money for growth” is too vague. “We need $85,000 for inventory tied to confirmed orders, expected customer payment within 45 days, with a 31% gross margin” is a lender-ready explanation.

For a general starting point, review Mehmi’s small business loan options for Canadian companies. If the need is operating cash, compare that with a working capital loan.

Granby’s local economy changes the financing conversation because lenders care about market conditions, business use, and repayment timing. A loan request should explain how the business fits the local environment.

First, Granby has an established industrial base. Granby Industriel says the industrial park has benefited from more than $1.8 billion of investment over the past 15 years and includes high-broadband fibre optic infrastructure, a large industrial footprint, and services suited to manufacturing and industrial operations. (Granby Industriel)

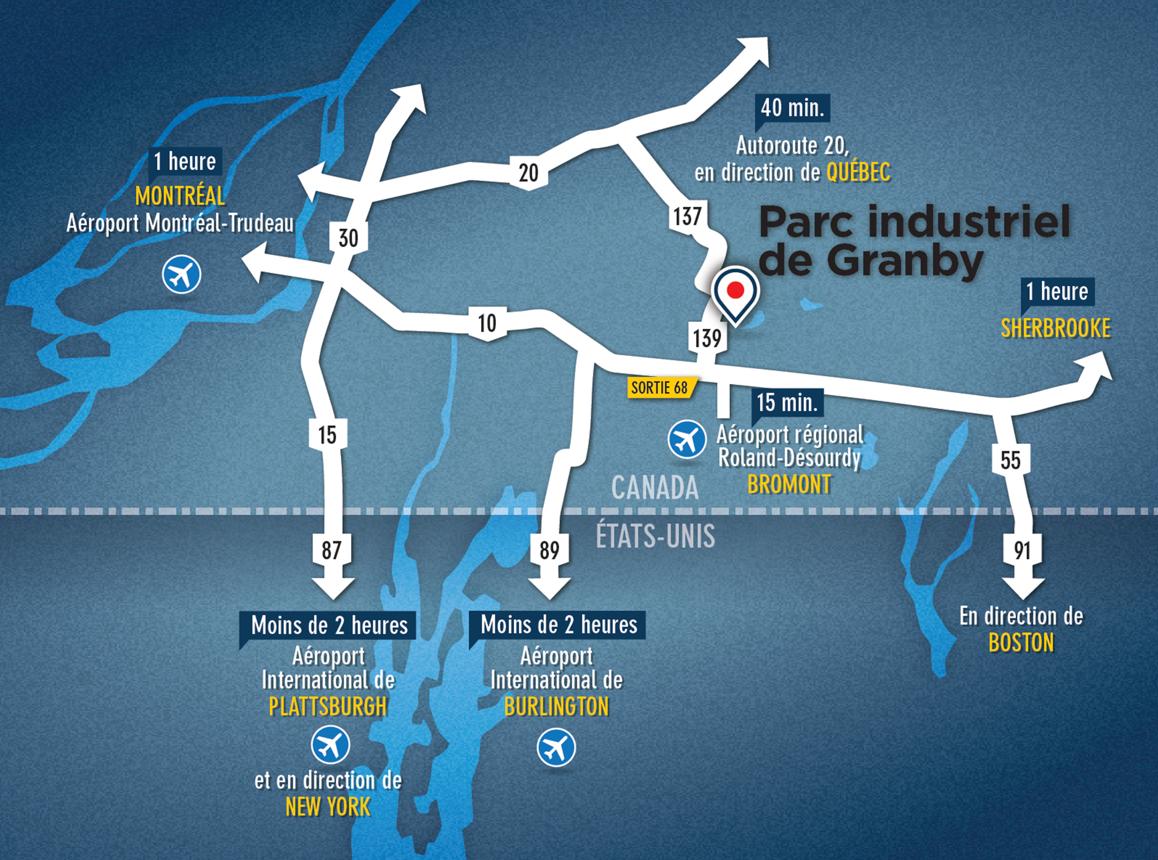

Second, location matters. Granby’s industrial park is accessed by Route 139 and Autoroute 10 at exit 68, and the “Invest in Granby” profile highlights proximity to Montréal, Sherbrooke, the U.S. border, and airports including Bromont, Montréal, Burlington, and Plattsburgh. (Granby Industriel) For local wholesalers, manufacturers, trucking-related businesses, food companies, and service firms, that can support regional customer reach.

Third, Granby has cross-regional customer potential. Granby Industriel states that four million consumers live within an 80-km radius of Granby and that the city is 65 km from the U.S. border at Vermont. (Granby Industriel) That can be helpful for retailers, suppliers, repair businesses, manufacturers, tourism-adjacent operators, and service companies, but it can also increase inventory and staffing demands before cash is collected.

Fourth, permits and municipal approvals affect timing. Ville de Granby’s permit page notes that permit or authorization applications can be submitted by owners, mandataries, contractors, and others depending on the request, and the city also provides online permits and forms. (Ville de Granby) For commercial or industrial work, Ville de Granby’s permit sheet states that a construction permit is required for construction, expansion, or transformation of a building. (Ville de Granby) If revenue depends on opening, renovating, installing signage, or modifying a space, the financing term should account for approval timing.

The best option depends on whether the need is one-time, recurring, invoice-driven, card-sales-driven, equipment-related, or property-related. The table below gives a practical comparison.

A business line of credit is usually better for repeated timing gaps. Invoice and freight factoring can help companies that sell to other businesses and wait 30, 45, or 60 days to get paid. A merchant cash advance may fit a Granby restaurant, retailer, or service business with consistent card sales, but owners should compare total cost carefully.

Start with the repayment source. The wrong repayment schedule can hurt even when the loan gets approved.

If the need is one-time and tied to a clear revenue event, a working capital loan may fit. If the need repeats every month or season, a line of credit is often safer. If the cash gap comes from unpaid invoices, factoring may be better than another fixed loan. If the business owns equipment, receivables, or inventory, asset-based lending may provide a more collateral-supported option.

Here is the practical opinion many owners do not hear early enough: the fastest money is not always the safest money. A fast approval with daily or weekly payments can make bank statements look weak if the repayment rhythm does not match deposits. A slightly slower structure that follows receivable timing or seasonality may protect the business better.

For a deeper Canada-wide view, read Mehmi’s guide to working capital loan options for Canadian small businesses.

If the financing need includes equipment, do not automatically use working capital to buy it. Long-life assets should usually be leased or financed over the period they generate revenue.

This matters in Granby because many local companies are asset-heavy: manufacturers, food processors, shops, distributors, contractors, clinics, restaurants, and service businesses. A CNC machine, forklift, delivery vehicle, compressor, refrigeration unit, packaging system, oven, dental chair, or point-of-sale system should not necessarily be paid from a short-term cash-flow facility.

A better structure may split the request. Use equipment leasing for machinery or tools, then use a smaller working capital facility for inventory, payroll, and launch costs. This keeps cash available for the operating cycle.

For broader asset planning, compare Mehmi’s equipment financing options and the guide to equipment leasing vs buying in Canada.

Lenders approve evidence, not excitement. A strong file shows how the money will be used, how repayment happens, and what protects the lender if the plan takes longer than expected.

The core underwriting framework is the 5Cs: character, capacity, capital, collateral, and conditions. A credit-risk reference describes 5C analysis as borrower character, repayment capacity, borrower capital at risk, collateral or guarantees, and the business/loan conditions.

In plain English:

Character is how the owner and business have handled obligations.

Capacity is whether cash flow can support the new payment.

Capital is how much owner equity or retained cash is in the business.

Collateral is what supports the facility if repayment fails.

Conditions include the industry, local market, interest-rate environment, seasonality, and use of funds.

Lenders also think in risk components: probability of default, exposure at default, and loss given default. That means they are asking: how likely is the business to miss payments, how much will be owing if it does, and how much could be recovered through collateral, guarantees, receivables, or equipment.

A complete file improves speed and credibility. Missing statements, unclear use of funds, or incomplete ownership details usually slow the process.

Prepare:

Recent business bank statements, usually three to six months.

Government ID for owners or guarantors.

Business registration, incorporation documents, or NEQ details.

Recent financial statements or year-to-date profit and loss, if available.

Aged accounts receivable and accounts payable, if invoices matter.

Current debt schedule showing balances and payments.

Lease, permit, signage, renovation, or zoning context if opening or expanding.

Equipment quotes, invoices, or asset lists if equipment supports the request.

A short use-of-funds summary.

The use-of-funds summary should answer five questions: how much is needed, what it buys, when revenue returns, what the repayment source is, and what happens if sales or receivables are slower than expected.

Québec business owners need to plan for GST and QST cash timing. The tax treatment can affect the size and structure of the financing request.

As of May 2026, CRA guidance says a GST/HST registrant can generally claim input tax credits for GST/HST paid on eligible expenses used only in commercial activities, subject to the rules and restrictions. (Canada) In Québec, Revenu Québec administers GST/HST and QST reporting, and registrants generally file a combined GST/HST-QST return for each reporting period. (Revenu Québec) Revenu Québec also discusses input tax credits and input tax refunds for registrants, including ITCs and ITRs for new registrants in respect of property on hand for commercial activities. (Revenu Québec)

The Québec-specific gotcha is timing. GST and QST may be recoverable or refundable in the right circumstances, but the cash can leave before recovery happens. If a Granby business is buying inventory, renovating, leasing equipment, paying contractors, or installing fixtures, the loan request should account for tax timing instead of assuming refunds are immediate.

For equipment-heavy requests, read Mehmi’s guide to GST/HST input tax credits on financed equipment in Canada and confirm Québec-specific QST treatment with your accountant.

Rates matter, but approval quality matters more. A lower rate with the wrong repayment schedule can still damage cash flow.

As of April 29, 2026, the Bank of Canada held the target overnight rate at 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%. (Bank of Canada) That does not tell you the exact rate for a Granby business loan because pricing also depends on credit profile, time in business, cash flow, security, term, repayment frequency, and lender appetite.

Stress-test the payment before signing. If the new payment is $6,500 per month, ask whether the business can still cover payroll, rent, GST/QST remittances, supplier terms, insurance, repairs, and owner draws during a slower month. If the answer depends on perfect sales, the amount, term, or product needs adjustment.

The Canada Small Business Financing Program can help eligible businesses access financing through participating lenders. It is useful to compare, but it is not automatic approval.

ISED says the Canada Small Business Financing Program makes it easier for small businesses to obtain financing from financial institutions by sharing risk with lenders. (ISED Canada) ISED’s guidelines cover eligibility, administration, and realization rules for CSBF loans and lines of credit. (ISED Canada)

For Granby businesses, CSBFP may fit equipment, leasehold improvements, working capital, intangible assets, or real property situations depending on the transaction. It still requires a lender, documentation, eligibility, and repayment capacity.

For a practical breakdown, use Mehmi’s Canada Small Business Financing Program guide. If the project involves a franchise, compare a franchise loan. If property is involved, compare commercial real estate financing.

Approval is not always the same as funding. Lenders may require certain items before advancing funds and may monitor the business afterward.

Conditions precedent are requirements that must be satisfied before the money is advanced. Examples include signed documents, proof of insurance, verified invoices, lien searches, landlord consent, permit confirmation, down payment proof, or payout statements.

Covenants are rules monitored after funding. A commercial lending reference explains that covenants are clauses that let a bank monitor business performance after funds are lent, while conditions precedent are requirements that must be met before funds are advanced. It also notes that prudent lenders prefer to identify warning signs before a missed payment occurs.

In real life, lenders watch for declining deposits, frequent overdrafts, NSF items, late tax remittances, unpaid suppliers, stale receivables, cancelled insurance, new high-cost debt, and ownership changes. A missed payment is usually a late warning sign, not the first one.

A Granby-area manufacturer had steady customers and a new purchase order from a larger buyer. The business was profitable, but cash was tight because it had to buy materials, schedule labour, and carry inventory before getting paid on 45-day terms.

The owner first asked for one $225,000 small business loan. The need was real, but the structure was too broad. About $95,000 was for materials and payroll timing, $80,000 was for production equipment, and $50,000 was a buffer for receivables.

The deal was reworked. The equipment portion was structured through a lease. The materials and payroll need became a smaller working capital facility. The receivable timing was supported through an invoice-based option for eligible customers.

The lender could now see the repayment logic. Equipment generated production capacity. Materials converted into shipped goods. Receivables converted into cash. The owner provided bank statements, customer history, supplier quotes, equipment details, and a short forecast.

From the underwriting side, the 5Cs lined up. Character was supported by clean repayment history. Capacity improved because the payment load was split properly. Capital remained in the business. Collateral came from the equipment and receivables. Conditions were supported by Granby’s manufacturing base and regional access.

The result was not just an approval. It was a structure the business could carry without starving operations.

A loan is not always the best solution. Sometimes the smarter move is to improve pricing, collect receivables faster, reduce overhead, lease assets properly, or fix tax compliance before borrowing more.

Be cautious if the money will cover repeated operating losses, owner draws the business cannot support, tax arrears without a go-forward plan, underpriced contracts, or stacked short-term debt. Borrowing can buy time, but it cannot fix a weak margin.

If the problem is slow receivables, consider factoring. If the problem is equipment cost, use leasing. If cash is trapped in owned assets, consider equipment refinancing or sale-leaseback. If the need is broad growth capital, compare Mehmi’s main business loan options.

The best next step is to package the request before applying. A lender should quickly understand the business, the amount, the use of funds, the repayment source, and the risk controls.

Create a one-page financing brief with your business overview, years operating, monthly revenue, current debt, requested amount, use of funds, customer base, collateral, repayment source, and timing. Add Granby-specific context where it helps: industrial park location, Route 139 and Autoroute 10 access, Montréal/Sherbrooke/U.S. border customer reach, manufacturing activity, permit timing, or expansion plans.

Mehmi can help compare working capital loans, lines of credit, factoring, merchant cash advances, equipment leasing, asset-based lending, CSBFP-supported options, and refinancing. The goal is not simply to get funded. The goal is to choose financing the business can still carry after the money arrives.

Granby businesses can compare working capital loans, lines of credit, invoice factoring, merchant cash advances, equipment leasing, asset-based lending, CSBFP-supported financing, commercial real estate financing, and franchise financing. The right option depends on purpose, repayment source, collateral, and timing.

Yes, but startups need stronger support. Lenders may ask for owner investment, industry experience, bank statements, projections, lease or permit details, personal credit, supplier quotes, and evidence of early sales or contracts. New businesses should avoid borrowing on a term that is shorter than the revenue ramp-up period.

Often, yes. If the asset will generate revenue over several years, leasing can protect cash better than using a short-term business loan. This is especially relevant for machinery, vehicles, restaurant equipment, medical equipment, shop tools, and production assets.

Yes. If your business sells to other businesses and waits 30, 45, or 60 days to collect, invoice factoring or invoice financing may fit better than a fixed-payment loan. Lenders will review customer quality, invoice aging, concentration, and whether invoices are valid and current.

Yes. GST and QST timing can affect cash flow, even when credits or refunds may be available. Québec businesses should plan tax cash flow carefully, especially for inventory, equipment, renovations, leaseholds, and operating expenses. Confirm treatment with an accountant.

The most common issue is unclear repayment capacity. Lenders may decline or reduce a request if bank deposits are inconsistent, debt payments are already high, margins are weak, tax arrears are unexplained, or the use of funds is vague. A clear file can materially improve the conversation.

.avif)