Learn how a working capital loan can help your small business manage cash flow, cover expenses, and fuel growth. Discover eligibility and application steps.

Running a small business is like walking a tightrope—every day brings new challenges, from covering payroll to paying suppliers on time. Even if your business is on the path to success, unpredictable sales cycles, late customer payments, and seasonal slowdowns can create cash flow gaps. A working capital loan can bridge those gaps, giving you the cash you need to keep operations smooth and seize growth opportunities.

At Mehmi Financial Group, we specialize in helping Canadian businesses access fast, flexible funding. Whether you need to cover day-to-day expenses or invest in marketing, a working capital loan can provide the cushion your company requires. This guide explains what working capital loans are, why they’re important, how they work, the benefits and drawbacks, and how to apply. By the end, you’ll understand how to use a working capital loan wisely to boost your business.

What Is a Working Capital Loan?

A working capital loan is a short-term financing solution designed to help businesses cover everyday operational costs. Unlike loans for fixed assets, working capital loans focus on cash flow rather than long-term investments. Common uses include:

Paying employee wages and payroll taxes

Purchasing inventory or raw materials

Covering rent, utilities, and insurance premiums

Handling unexpected expenses, such as equipment repair or emergency supplier invoices

Most working capital loans are unsecured, meaning you don’t have to pledge equipment or property as collateral. Instead, lenders typically evaluate your company’s monthly revenue, credit history, and overall financial health.

Why Are Working Capital Loans Important?

Small businesses often face fluctuating revenue. Even profitable companies can struggle when:

Sales Slow Down Seasonally: Retailers may see peak sales in holiday seasons and much lower revenue in winter.

Customers Pay Late: A five-figure invoice that takes 60 days to clear can create a temporary cash crunch.

Unexpected Expenses Arise: Repairs, urgent supply orders, or emergency hires can eat into reserves.

A working capital loan steps in when your income doesn’t align with expenses. Instead of dipping into personal savings or skipping vendor payments, you can borrow a short-term amount to maintain smooth operations. This financial cushion ensures you can:

Cover rent, utilities, and insurance without delay

By stabilizing cash flow, working capital loans help your business run efficiently—even during slow months—and allow you to seize growth opportunities when they arise.

Benefits of Working Capital Loans

1. Quick Access to Cash

Many working capital lenders—especially online or alternative financing providers—offer approval and funding in as little as 24–72 hours. This speed is crucial when you need to pay bills, suppliers, or employees without delay.

2. Flexible Use of Funds

Unlike loans designated for equipment or real estate, working capital loans can be used for virtually any business expense:

Payroll and staff bonuses

Inventory and raw materials

Utility bills and rental deposits

Short-term marketing campaigns or promotions

This flexibility ensures you address the most pressing needs without restrictions.

3. Unsecured Options

Because working capital loans often don’t require collateral, you don’t have to pledge assets like machinery or property. This makes it easier for newer businesses or those without significant owned assets to qualify.

4. Helps Fuel Growth

If you receive a large bulk order or want to launch a targeted advertising campaign, a working capital loan can provide the extra funds needed to capitalize on those opportunities. By bridging the gap between expenses and revenue, you can scale operations more confidently.

5. Improved Cash Flow Management

Rather than paying vendors late or dipping into emergency funds, working capital loans smooth out cash flow fluctuations. You can cover short-term obligations on time, maintain strong credit relationships, and avoid late fees or penalties.

How Do Working Capital Loans Work?

While specifics vary by lender, most working capital loans follow similar steps:

Application and Pre-Qualification

You complete a short online form or paper application.

Lenders review your business’s monthly revenue, credit score (both personal and, if available, business), and time in operation.

Many online lenders provide pre-qualification within minutes without a hard credit inquiry, giving you an estimate of loan amounts and rates.

Documentation Requirements

Financial Statements: Recent bank statements (often 3–6 months) and a basic Profit & Loss summary.

Tax Returns: Business or personal tax returns (usually the last two years).

Identification: Government-issued ID and Social Insurance Number (SIN).

If offered as collateral, equipment or real estate details may be required, but most working capital loans are unsecured.

Loan Approval

The lender offers you a loan amount based on your revenue and credit profile.

Interest rates vary widely—online lenders might charge 10–30% APR, while credit unions or traditional banks could offer lower rates (8–15% APR) if you have strong credit.

Funds Disbursement

Once you accept the offer, funds are usually deposited into your business bank account within 1–3 business days.

Some lenders transfer funds even faster—within 24 hours—especially if your application is complete and documentation is in order.

Repayment

Traditional Working Capital Loans: Fixed monthly payments over a short term (6–18 months).

Lines of Credit: Repay and redraw up to your credit limit; interest accrues only on the outstanding balance.

Merchant Cash Advances (MCA): The lender advances you a lump sum, and you repay via a percentage of daily credit card sales. MCAs can be risky due to high factor rates.

Completion and Renewal

Once the loan is repaid, you can apply for another working capital loan or maintain a revolving line of credit for ongoing cash flow needs.

Continuously meeting repayment schedules improves your business’s credit profile, enabling better terms on future borrowing.

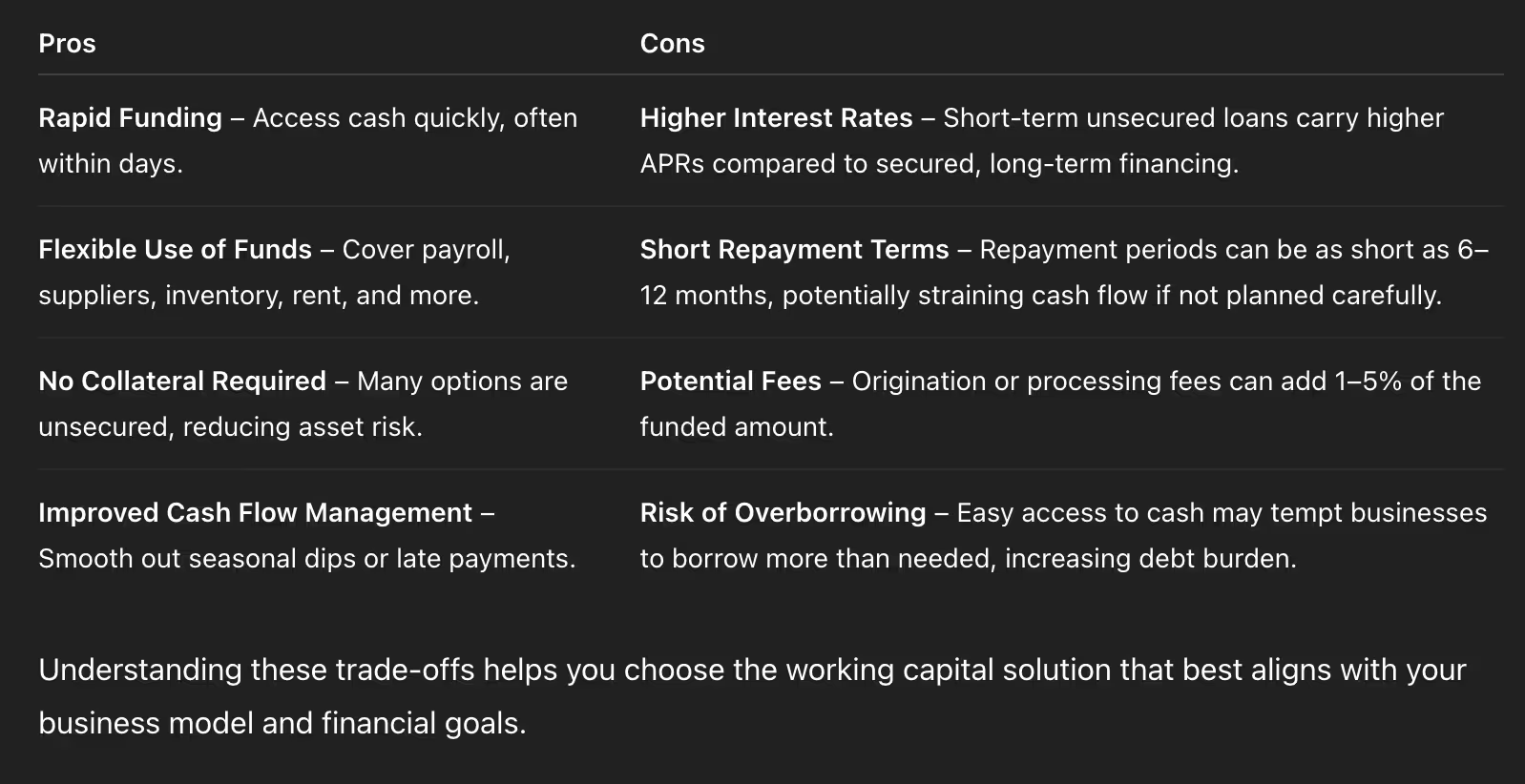

Pros and Cons of Working Capital Loans

Understanding these trade-offs helps you choose the working capital solution that best aligns with your business model and financial goals.

How to Get a Working Capital Loan

Step 1: Assess Your Financing Needs

Calculate Short-Term Expenses: Determine exactly how much cash you need—whether for payroll, inventory, or rent—plus a buffer (typically 10–20% extra).

Choose the Right Product: Decide if a term loan, line of credit, or merchant cash advance is best. If you need ongoing flexibility, a line of credit may make sense. For one-off expenses, a short-term loan might be more cost-effective.

Step 2: Check Your Credit Scores

Personal Credit Score: If you’re a sole proprietor or early-stage startup, lenders use your personal credit. Aim for a score of 650 or higher for favorable rates.

Business Credit Score: If your company has been operating for at least a year, lenders may also review your business credit profile. The higher, the better.

Step 3: Gather Required Documentation

Prepare these documents in PDF format to speed up the process:

Latest Bank Statements: 3–6 months, showing consistent deposits and cash flow.

Profit & Loss Statement: A simple summary of revenue and expenses for the past 12 months.

Tax Returns: Personal and/or business tax returns for the last two years.

Identification: Government-issued photo ID (driver’s license or passport) and Social Insurance Number (SIN).

Business Registration: Articles of incorporation or business license (if applicable).

Having these ready before you apply ensures a smoother and faster approval process.

Step 4: Compare Lenders and Pre-Qualify

Traditional Banks: Offer lower interest rates (8–12% APR) but require strong credit (650+), at least one year in business, and sometimes collateral. Approval may take 1–2 weeks.

Credit Unions: Can be more flexible with credit requirements and offer competitive rates (8–15% APR). Approvals generally happen in 3–5 business days.

Online Lenders: Provide rapid funding (often 24–72 hours) with minimal documentation. Credit score requirements can be as low as 600, but APRs range from 10–30%.

Merchant Cash Advances: Approval in 1–2 days; funds delivered in 24 hours. Rates are high—often 25–50% effective, depending on factor rates. Best for extremely short-term cash needs if other options are unavailable.

Pre-qualify with multiple lenders to compare rates and terms without affecting your credit. Mehmi Financial Group can help you evaluate offers and choose the best option.

Step 5: Submit a Complete Application

Accurate Information: Fill out every field correctly to avoid delays.

Upload Documents: Label each file (e.g., “Bank_Statements_March-May_2024.pdf”).

Provide a Simple Explanation: Briefly state how you will use the funds (e.g., “$15,000 for payroll and $5,000 for inventory”).

Step 6: Respond Promptly to Follow-Up Requests

After you submit, lenders may ask for additional details—such as updated bank statements or clarification on your cash flow projections. Respond within 24–48 hours to speed up approval.

Step 7: Review & Sign the Loan Agreement

Confirm Loan Details: Verify the principal amount, APR, term length, and repayment schedule.

Check Fees & Penalties: Look for origination fees (typically 1–5% of the loan), late-payment fees, and any prepayment penalties.

Sign Electronically: Many lenders offer e-signature options for quick turnaround. If a paper signature is required, scan and email back promptly.

Step 8: Receive Funds & Implement Your Plan

Funds Disbursement: Most working capital loans deposit into your bank account within 1–3 business days. Merchant cash advances may fund within 24 hours.

Use Funds Wisely: Allocate funds strictly to intended purposes—payroll, inventory, or rent—while maintaining meticulous records for post-disbursement verification.

FAQ for Working Capital Loans

1. How is a working capital loan different from other types of business loans? A working capital loan specifically targets day-to-day operational expenses—such as payroll, inventory, and utilities—rather than long-term investments like real estate or equipment. In contrast, term loans often finance large fixed assets, and equipment financing is secured by the asset being purchased.

2. Who qualifies for a working capital loan? Qualification criteria vary by lender but generally include:

Credit Score: Personal score of 650+ or business credit score of 75+ for unsecured loans.

Time in Business: Many lenders prefer at least 6–12 months of operation. Some online lenders approve startups more quickly.

Revenue: Consistent monthly revenue (often $5,000+ per month) for at least 3–6 months.

Documentation: Recent bank statements, Profit & Loss statements, and tax returns.

Even if you have fair credit or limited time in business, alternative lenders and credit unions can provide flexible options tailored to your needs.

3. What are the benefits of using a business line of credit versus a short-term loan?

Flexibility: A line of credit allows multiple withdrawals and repayments up to a set limit. You only pay interest on the funds you use.

Ongoing Access: As you repay, your available credit replenishes, creating a continuous buffer for cash flow fluctuations.

Variable Interest Rates: Often tied to prime rates, so costs can fluctuate compared to fixed short-term loan rates.

Short-term loans provide a lump sum you repay in fixed installments, ideal for one-time expenses. Lines of credit are better for ongoing needs and unpredictable cash flow demands.

Soft Call to Action

If you need fast, flexible funding to cover payroll, restock inventory, or navigate a slow season, Mehmi Financial Group can help you secure the right working capital solution. From competitive lines of credit and term loans to specialized invoice factoring, we partner with over 30 lenders to find the best terms for your business.

.avif)